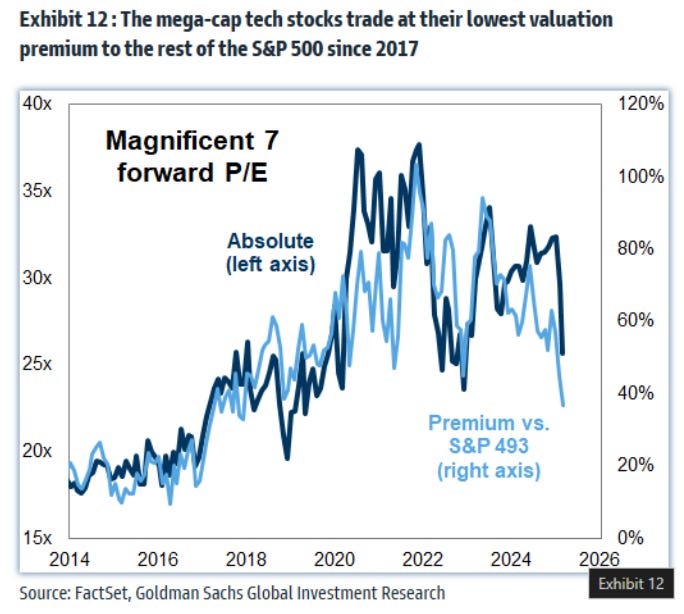

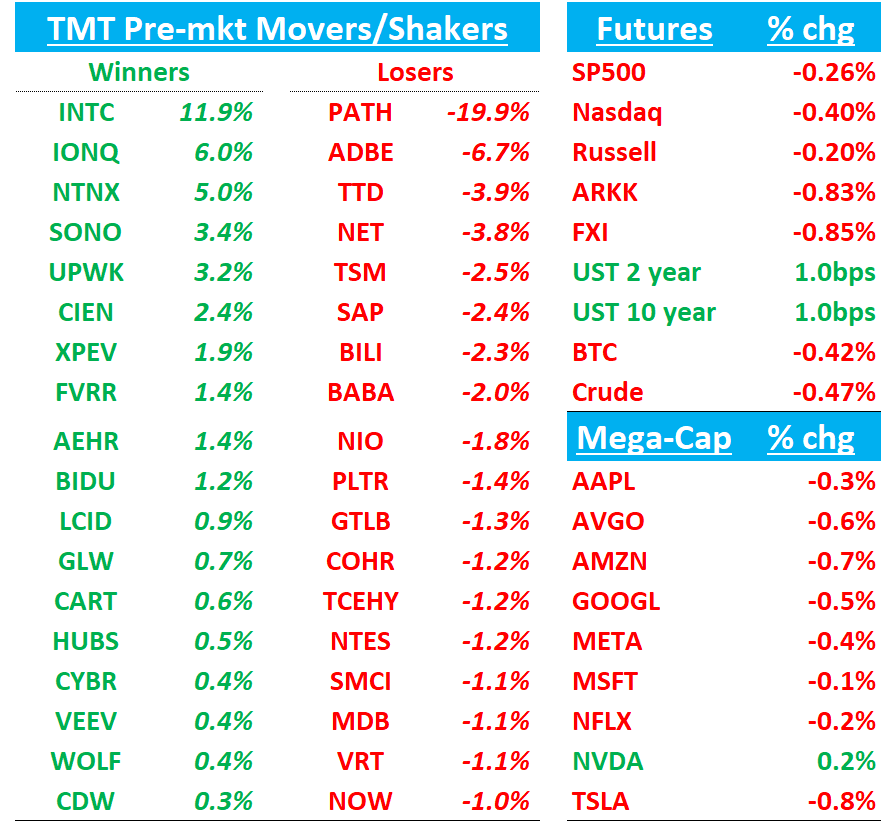

TMTB Morning Wrap TMTB 晨报摘要

QQQs -35bps; BTC flat; China -1%.

QQQs 下跌 35 个基点;BTC 持平;中国下跌 1%。

QQQs 下跌 35 个基点;BTC 持平;中国下跌 1%。

QQQs -35bps; BTC flat; China -1%. PPI came in a bit cooler than expected, flat m/m vs street at +0.3%.

QQQs 下跌 35 个基点;BTC 持平;中国下跌 1%。PPI 数据略低于预期,环比持平,而市场预期为+0.3%。

Let’s get straight to it…

让我们直奔主题…

Not much to write home about; every q that passes without a significant change in the AI narrative for ADBE makes the bears feel more emboldened — mgmt sounded unexcited on the call imo. In other words: a lack of narrative change in the bull (valuation - 19x CY26 EPS and AI traction just starting) vs bear (structural AI loser, competition) debate favors the bears right now. Bears also hooked onto limiting disclosures from ADBE as they will only update the new ARR AI line item line “periodically” and not “quarterly” ($125M this q, $250M by YE) although they are providing some new details in terms of segmenting the corporate / enterprise business vs. the consumer / creative business. Despite NN ARR DM coming in-line, RPO and bookings missed widely (bookings $5.53B vs expectations for $6B+) and cRPO growth of 12% decelerated from 16% in Q4, likely from enterprise softness. ADBE didn’t specifically say much about the macro (tariffs, trade wars, consumer tightened) but highlighted structural digital tailwinds, diverse biz and no direct tariff exposure. ADBE summit on the 17th next week.

没什么值得大书特书的;每一季度过去,如果 ADBE 的 AI 叙事没有显著变化,熊市情绪就会更加高涨——在我看来,管理层在电话会议中表现得并不兴奋。换言之,在多头(估值——19 倍 CY26 每股收益,AI 吸引力刚开始显现)与空头(结构性 AI 输家,竞争)的辩论中,缺乏叙事变化目前对空头有利。空头还抓住了 ADBE 披露信息有限这一点,因为他们只会“定期”而非“季度性”更新新的 ARR AI 项目(本季度 1.25 亿美元,年底 2.5 亿美元),尽管他们在区分企业/企业业务与消费者/创意业务方面提供了一些新细节。尽管 NN ARR DM 符合预期,但 RPO 和预订量大幅低于预期(预订量 55.3 亿美元,预期为 60 亿美元以上),且 cRPO 增长从第四季度的 16%放缓至 12%,可能源于企业业务疲软。ADBE 没有具体提及宏观环境(关税、贸易战、消费者紧缩),但强调了结构性数字顺风、业务多元化以及无直接关税影响。ADBE 峰会定于下周 17 日举行。

ADBE RESULTS: Q1 ADBE 财报:第一季度

- ADJ EPS $5.08 vs. $4.48 y/y, EST $4.97

- ADJ 每股收益(EPS)5.08 美元,去年同期为 4.48 美元,预期(EST)4.97 美元

- Revenue $5.71B, +10% y/y, EST $5.66B

- 营收 57.1 亿美元,同比增长 10%,预期 56.6 亿美元

- Digital experience revenue $1.41B, +9.3% y/y, EST $1.4B

- 数字体验收入 14.1 亿美元,同比增长 9.3%,预估 14 亿美元

- Subscription revenue $5.48B, +12% y/y, EST $5.42B

- 订阅收入 $5.48B,同比增长 +12%,预估 $5.42B

- Product revenue $95M, -20% y/y, EST $95.4M

- 产品收入 9500 万美元,同比下降 20%,预估 9540 万美元

- R&D expenses $1.03B, +9.3% y/y, EST $1.01B

- 研发费用 $1.03B,同比增长 9.3%,预期 $1.01B

- ADJ operating income $2.72B, +10% y/y, EST $2.66B

- ADJ 营业收入$2.72B,同比增长 10%,预估$2.66B

- Services and other revenue $136M, -7.5% y/y, EST $144.3M

- 服务及其他收入 $136M,同比下降 7.5%,预期 $144.3M

GUIDANCE: Q2

- Guides ADJ EPS $4.95 to $5.00, EST $5.00

- 指引调整后每股收益(ADJ EPS)为$4.95 至$5.00,预估(EST)为$5.00

- Guides revenue $5.77B to $5.82B, EST $5.8B

- Guides revenue $5.77B 至 $5.82B,预估 $5.8B

- Guides digital media revenue $4.27B to $4.30B, EST $4.28B

- 预计数字媒体收入为 42.7 亿美元至 43.0 亿美元,预期 42.8 亿美元

- Guides digital experience revenue $1.43B to $1.45B, EST $1.45B

- 指导数字体验收入为 14.3 亿美元至 14.5 亿美元,预估为 14.5 亿美元

- Guides Digital Experience subscription revenue $1.32B to $1.33B, EST $1.33B

- Guides Digital Experience 订阅收入预计为 13.2 亿至 13.3 亿美元,预估为 13.3 亿美元

S: Another disappointing q and guide. 4Q financials relatively in-line, but ARR of $920.1mn missed St at $921mn, and guided 1Q Rev growth of 22.3% vs cons 26.4% & FY growth of 22.9% vs cons 25.7%. NNARR guided to $200M vs street at $215M and called out demand risks: “we're mindful of macroeconomic conditions, deal timing, and federal spending uncertainty” as well as a $10M F26 ARR hit from the sunsetting of their deception product. Bears will also hate that mgmt was talking up the growth quarter intra-q and just whiffed - no one likes to be walked off a cliff.

S: 又一次令人失望的季度和指引。第四季度财务数据相对符合预期,但 ARR 为 9.201 亿美元,低于市场预期的 9.21 亿美元,且指引第一季度收入增长 22.3%,低于市场预期的 26.4%,全年增长指引为 22.9%,低于市场预期的 25.7%。NNARR 指引为 2 亿美元,低于市场预期的 2.15 亿美元,并指出了需求风险:“我们注意到宏观经济状况、交易时机以及联邦支出的不确定性”,此外,其欺骗产品停用将对 F26 ARR 造成 1000 万美元的冲击。管理层在季度内还在谈论增长季度,结果却令人失望,空头也会对此感到不满——没人喜欢被推下悬崖。

Bulls will try to hand their hats on a 4x C26 EV/sales multiple and 20% rev/ARR growth and say new CFO means guide was conservative although bears will push back there’s not much FCF support and its a single product company which is deserving of a low multiple.

多头将试图以 4 倍 C26 EV/销售额倍数和 20%收入/ARR 增长为依据,并称新 CFO 意味着指引较为保守,尽管空头会反驳称自由现金流支持不多,且其为单一产品公司,应享有较低倍数。

PATH: 1st top line miss as public co and Q1/FY26 guided well below street. 1Q ARR to 11% vs cons +13%. Guiding to 10% ARR growth for FY25, below street at 13-14%. Mgmt did not sound great on the call and called out DOGE as a specific headwind. Stock had been shorted given these fears along with AI disruption risk.

PATH: 首次公开公司一季度业绩低于预期,且 FY26 第一季度指引远低于市场预期。一季度 ARR 增长 11%,而市场共识为 13%。FY25 ARR 增长指引为 10%,低于市场预期的 13-14%。管理层在电话会议中的表现并不出色,并特别指出 DOGE 为具体阻力。由于这些担忧以及 AI 颠覆风险,该股已被做空。

Key quotes: 关键引述:

“while we remain optimistic about the long-term opportunity in the US Public sector, the ongoing transition has created short-term uncertainty for deal closures, and we have factored this into our guidance for fiscal 2026 with a more pronounced impact in the first half of the year.”

“尽管我们对美国公共部门的长期机遇保持乐观,但持续的转型给交易完成带来了短期的不确定性,我们已将此纳入 2026 财年的指引中,预计上半年将受到更为显著的影响。”“There has also been a significant increase in volatility in the overall macroeconomic environment, particularly in the last two weeks. In recent discussions with customers, the external environment has created uncertainty around their budgets. Foreign exchange rates have also significantly fluctuated over the last week. Given these trends, we are taking a measured approach for fiscal 2026, adding additional prudence to our overall guidance given the volatile environment”

“整体宏观经济环境的波动性显著增加,尤其是过去两周。在最近与客户的讨论中,外部环境给他们的预算带来了不确定性。过去一周,外汇汇率也出现了大幅波动。鉴于这些趋势,我们对 2026 财年采取了审慎的态度,在波动环境下为整体指引增加了额外的谨慎性。”

Gets a dg at BofA: BofA downgraded UiPath to Underperform from Neutral with a price target of $10, down from $18, following the company's "disappointing" FY26 outlook. Macro pressure in the Federal vertical was cited, though commentary suggests that pressure is more broad-based and "unlikely to abate soon," says the analyst, who sees few catalysts for the shares, even at current level.

在 BofA 获得降级:BofA 将 UiPath 评级从中性下调至表现不佳,目标价从 18 美元降至 10 美元,此前该公司公布了“令人失望”的 2026 财年展望。分析师指出,联邦垂直领域的宏观压力被提及,但评论表明这种压力更为广泛且“不太可能很快缓解”,认为即使当前水平,该股也缺乏上涨催化剂。

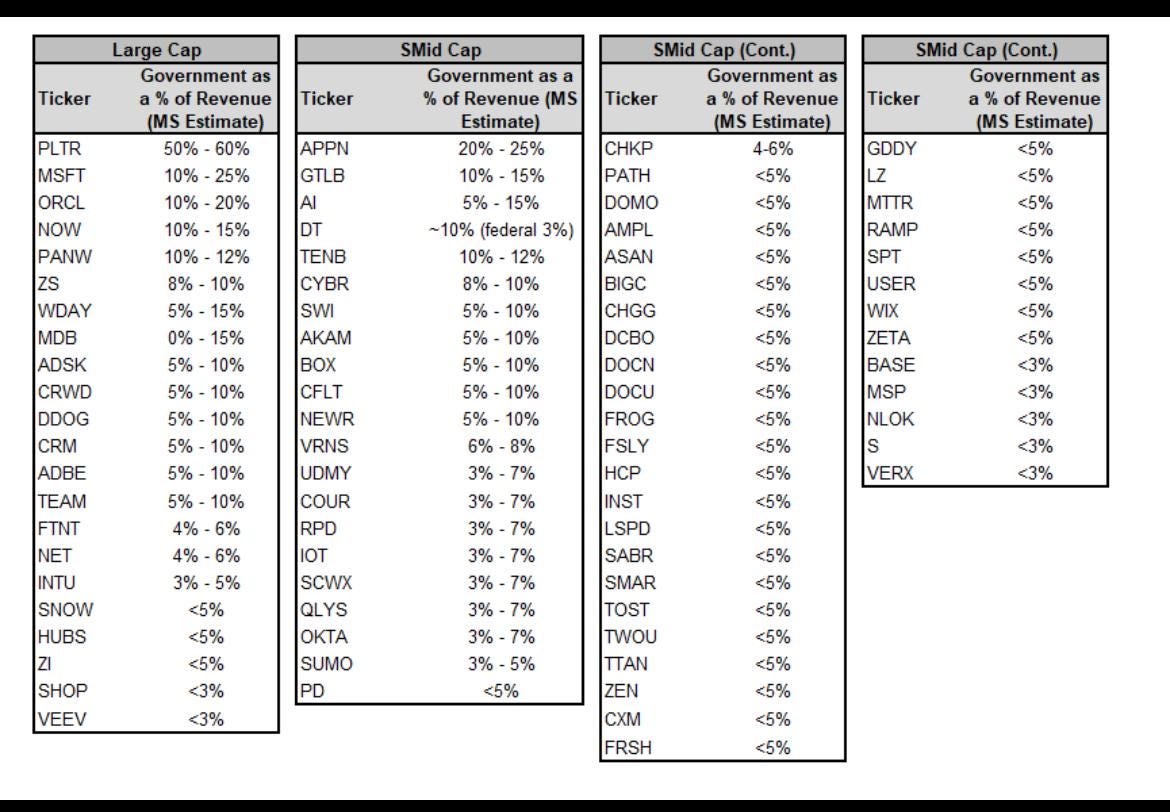

Reminder, Federal Exposure in SW. From MS:

提醒,联邦政府在 SW 中的敞口。来自 MS:

ABNB: BofA says AirDNA estimates in Feb 9% y/y a decel vs Jan at 19% y/y. AirDNA now estimates 7% y/y for the full q, below street at 8%….M Science notes on ABNB this AM that “Volume growth has been sequentially weaker in the U.S. over the past three weeks.”

ABNB:美国银行表示,AirDNA 估计 2 月同比增长 9%,较 1 月的 19%同比增速有所放缓。AirDNA 目前预计整个季度同比增长 7%,低于市场预期的 8%……M Science 今早关于 ABNB 的评论指出,“过去三周内,美国的成交量增长逐周减弱。”

RBLX: Another uptick in weekly data at Yipit, with hours engaged/DAUs tracking 7-8 ppts above street. March 10ppts accel vs Feb so far.

RBLX:Yipit 周数据显示,用户参与时长/日活跃用户数继续上升,超出市场预期 7-8 个百分点。与二月相比,三月至今的增速加快了 10 个百分点。

SHOP: Yipit says Q1 GPV ex PYPL trending to 28-30% vs street at 31%, slowing in Feb due to leapwind.

SHOP: Yipit 表示第一季度剔除 PYPL 后的 GPV 趋势为 28-30%,而市场预期为 31%,由于闰年效应,二月增速放缓。

TTD: Downgraded to Neutral at Cleveland (will pass along deets when i get in the chat)

TTD:在 Cleveland 被下调至中性评级(等我进入聊天室后会传递详细信息)

ROKU: M-sci mixed saying engagement healthy in Q1, but has come down from record highs im Q4

ROKU: M-sci 混合表示第一季度参与度健康,但已从第四季度的历史高点回落

The hire that most bulls hoped for - product execution or sale odds go up as lots of fat still to cut at INTC, but bears will say this is worst outcome as best outcome is for them give up and split co where a new well respected CEO who wants to try organic turnaround is just false hope (the letter sounds like a continuation of Pay’s strategy). Back in August, he reportedly wanted to cut a LOT of headcount: Reuters.

大多数多头期待的人选——产品执行或出售的几率增加,因为英特尔(INTC)仍有大量成本可削减,但空头会认为这是最坏的结果,因为对他们来说,最好的结果是公司放弃并分拆,一位备受尊敬、希望尝试有机转型的新 CEO 不过是虚假的希望(这封信听起来像是 Pay 策略的延续)。早在八月,据路透社报道,他曾希望大幅裁员。

Key quotes from PR PR 的关键引述

· “Together, we will work hard to restore Intel’s position as a world-class products company, establish ourselves as a world-class foundry and delight our customers like never before…Past achievements do not predict future success, especially in an industry as dynamic as ours. The pace of change continues to accelerate, and the competition is intense…Be nimble and self-assess. Anchor yourself in these core beliefs: “Stay humble, work hard, delight our customers…Under my leadership, Intel will be an engineering-focused company. We will push ourselves to develop the best products, listen intently to our customers and hold ourselves accountable to the commitments we make so that we build trust.”

· “我们将共同努力,致力于恢复英特尔作为世界级产品公司的地位,确立我们作为世界级代工厂的地位,并以前所未有的方式取悦我们的客户……过去的成就并不能预示未来的成功,尤其是在我们这个如此充满活力的行业中。变化的速度持续加快,竞争异常激烈……保持敏捷并自我评估。以这些核心信念为锚:‘保持谦逊,努力工作,取悦我们的客户……在我的领导下,英特尔将成为一个以工程为核心的公司。我们将推动自己开发最好的产品,认真倾听客户的声音,并对我们所做的承诺负责,从而建立信任。’”

Street generally positive with an upgrade at BofA. A few snippets:

华尔街普遍看好,因美国银行(BofA)上调评级。部分要点:

BofA upgrades INTC to Neutral from Underperform with a new $25 PO (from $19) on 28x CY26E P/E. BofA likes the new CEO appointment of Lip-Bu Tan (effective March 18) given his successful track record at Cadence (32x stock appreciation vs SOX 16x), prior INTC board experience, and broad industry relationships as Walden International VC Chairman. BofA believes INTC has greater restructuring opportunity under Tan's leadership, with strong enterprise CPU incumbency increasing chances of success. They note improving conditions might enable divestiture of Altera and automotive assets, deleveraging the balance sheet. BofA also flags unconfirmed media reports about a potential TSMC joint venture to operate INTC's foundry division with fabless companies, which could support turnaround efforts if materialized.

BofA 将 INTC 评级从表现不佳上调至中性,并将目标价从 19 美元上调至 25 美元,基于 28 倍的 2026 年预期市盈率。BofA 对 Lip-Bu Tan 的新任 CEO 任命表示赞赏(自 3 月 18 日起生效),鉴于他在 Cadence 的成功记录(股票升值 32 倍,而 SOX 为 16 倍)、此前在 INTC 董事会的经验以及作为华登国际 VC 主席的广泛行业关系。BofA 认为在 Tan 的领导下,INTC 有更大的重组机会,强大的企业 CPU 地位增加了成功的机会。他们指出,改善的条件可能使 Altera 和汽车资产的剥离成为可能,从而降低资产负债表杠杆。BofA 还提到未经证实的媒体报道,关于台积电可能与无晶圆厂公司合资运营 INTC 的晶圆代工部门,如果实现,这可能支持扭亏为盈的努力。

Wells Fargo analyst Aaron Rakers reiterated an Equal Weight rating and $25 price target on Intel after the company named Lip Bu-Tan as its next CEO. The firm is positive on the announcement as the company looks to reshape or accelerate the validation of its Foundry strategy. While the hiring of Tan is extremely notable in and of itself, the move in Intel shares is likely being driven by views of the new CEO's openness to consider broader strategic moves, for example a pro-spin or accelerating corporate actions, the analyst tells investors in a research note.

富国银行分析师 Aaron Rakers 重申对英特尔的“中性”评级和 25 美元的目标股价,此前该公司任命 Lip Bu-Tan 为下一任 CEO。该公司对此次任命持积极态度,因为英特尔正寻求重塑或加速其代工战略的验证。尽管 Tan 的聘用本身非常引人注目,但英特尔股价的波动可能受到市场对新 CEO 考虑更广泛战略举措(例如支持分拆或加速企业行动)的开放态度的看法驱动,该分析师在研究报告中告诉投资者。

After Intel announced that former Cadence CEO and former Intel board member Lip-Bu Tan will become CEO, Morgan Stanley analyst Joseph Moore said the firm is "going to avoid rushing to judgement - we did that the last time - but directionally it does seem like a good outcome." While the company's "quick and decisive actions around the CEO decision is a good start," the company's headwinds remain significant, as slippage in the server roadmap, the lack of a near-term AI offering, a very competitive client CPU market, and over $10B in 12-month trailing losses in the foundry business leave the company with near-term challenges that have "no quick fix," the analyst added. Morgan Stanley maintains an Equal Weight rating and $25 price target on Intel shares.

在英特尔宣布前 Cadence 首席执行官、前英特尔董事会成员陈立武将出任 CEO 后,摩根士丹利分析师 Joseph Moore 表示,该公司“将避免仓促下结论——我们上次就是这样做的——但从方向上看,这似乎是一个不错的结果。”尽管该公司“在 CEO 决策上的迅速和果断行动是一个良好的开端”,但该公司的逆风依然显著,由于服务器路线图的延误、缺乏近期的 AI 产品、竞争激烈的客户端 CPU 市场,以及晶圆代工业务在过去 12 个月中超过 100 亿美元的亏损,使得该公司面临“无法快速解决”的短期挑战,分析师补充道。摩根士丹利维持对英特尔股票的“中性”评级和 25 美元的目标价。

TD Cowen maintains Buy and $46 PT on Pinterest after speaking with a digital ad agency ($4B+/yr managed spend) about PINS' Performance+ suite. The agency reports 80% of their active Pinterest advertisers are using Performance+ features, with Performance+ Creative driving a 19% lift in checkout revenue. Cowen highlights that the Performance+ ROAS bidding tool (launching fully in 1Q25) is significantly improving prospecting for a major client, who now uses it as their sole Pinterest prospecting strategy in the US. Performance+ Creative offers GenAI tools particularly beneficial for smaller brands without resources for Pinterest-optimized content. Cowen is incrementally more positive on Performance+ supporting mid-to-high teens revenue growth for PINS throughout 2025.

TD Cowen 在与一家数字广告机构(年管理支出超过 40 亿美元)就 Pinterest 的 Performance+套件进行交流后,维持对 Pinterest 的买入评级和 46 美元目标价。该机构报告称,其活跃的 Pinterest 广告主中有 80%正在使用 Performance+功能,其中 Performance+ Creative 推动结账收入提升了 19%。Cowen 强调,Performance+的 ROAS 竞价工具(将于 2025 年第一季度全面推出)正在显著改善一位主要客户的潜在客户挖掘,该客户现在将其作为在美国的唯一 Pinterest 潜在客户挖掘策略。Performance+ Creative 提供的生成式 AI 工具特别适合没有资源制作 Pinterest 优化内容的小品牌。Cowen 对 Performance+支持 Pinterest 在 2025 年全年实现中高两位数收入增长持更加积极的态度。

DA Davidson upgraded Microsoft to Buy from Neutral with a price target of $450, up from $425, as the firm believes the company has moved to a more rational capex strategy and is "the best positioned Mag6 for a slowing consumer." Microsoft has been the worse performing Mag6 member in the six months since the firm's previous downgrade, notes the analyst, who believes that shares now "properly reflect" the drag from previous capital expenditure escalation since the company has provided guidance for flat sequential capex over the next couple of quarters and lower growth into FY26.

DA Davidson 将微软评级从中性上调至买入,目标价从 425 美元上调至 450 美元,因为该公司认为微软已转向更合理的资本支出策略,并且是“面对消费者放缓的最佳 Mag6 成员”。分析师指出,自该公司上次下调评级以来的六个月中,微软一直是表现最差的 Mag6 成员,但他认为,由于微软已提供未来几个季度资本支出持平的指引,并预计到 FY26 年增长放缓,股价现在“恰当地反映”了此前资本支出增加的拖累。

What are AI Bulls playing for on Tencent? Bulls think Tencent is most similar to META around how they will benefit from AI, with high margin advertising as a Gen AI leader: Tencent has China's most resourceful data, capturing 30% of total internet user time through 1.1bn Weixin users and diverse platforms. Tencent integrated DeepSeek into WeChat, Yuanbao AI assistant, QQ Music and Tencent Maps in mid-February. Bulls think targeting China's advertising ) and retail/ecommerce TAMs, Tencent could see faster EPS revisions from high-margin advertising versus BABA's single-digit margin AI cloud business.

腾讯的 AI 多头在押注什么?多头认为,腾讯在如何从 AI 中获益方面与 META 最为相似,作为生成式 AI 的领军者,其高利润广告业务将带来显著收益:腾讯拥有中国最具价值的数据资源,通过 11 亿微信用户及多元化平台,占据了互联网用户总时长的 30%。2 月中旬,腾讯已将 DeepSeek 整合进微信、元宝 AI 助手、QQ 音乐及腾讯地图。多头认为,瞄准中国的广告及零售/电商总市场规模(TAM),相较于阿里巴巴(BABA)个位数利润率的 AI 云业务,腾讯可能因高利润广告业务而实现更快的每股收益(EPS)修订。

Jefferies assesses CPO (Co-Packaged Optics) impact on key companies: NVDA's position as full system provider gives strategic advantage during technological transitions; AVGO is the CPO technology industry leader, well-positioned for both near-term Scale-Up transition from passive copper and long-term front-end CPO-based switching; MRVL faces highest disruption potential given its 75% DSP market share, as new optical technologies like LRO/LPO/CPO focus on removing DSPs; sentiment remains negative for COHR/LITE due to transceiver loss in CPO architectures, though they'll still supply Laser/ELS components in CPO (revenue headwind but with higher 50-60% gross margins vs 25-30%).

Jefferies 评估 CPO(共封装光学)对关键公司的影响:NVDA 作为全系统提供商的地位在技术转型期间具有战略优势;AVGO 是 CPO 技术行业的领导者,无论是在从被动铜缆向近期 Scale-Up 过渡还是长期基于前端 CPO 的交换方面都处于有利位置;MRVL 因其 75%的 DSP 市场份额面临最高的颠覆风险,因为 LRO/LPO/CPO 等新光学技术旨在移除 DSP;由于 CPO 架构中收发器的损失,COHR/LITE 的情绪仍然负面,尽管它们仍将在 CPO 中供应激光器/ELS 组件(收入受阻,但毛利率更高,为 50-60%,而之前为 25-30%)。

Citi analyst Asiya Merchant opened a "90-day positive catalyst watch" on shares of Corning while keeping a Buy rating on the name with a $58 price target into the investor day on March 18. In addition to updates on various end markets, the firm expects management to highlight the optical segment business, which is benefitting from secular and cyclical demand trends with carrier demand for fiber normalizing to build trends. Citi believes Corning's risk/reward screens favorable given its improving demand and free cash flow generation potential.

花旗分析师 Asiya Merchant 对康宁股票开启了“90 天积极催化剂观察”,同时维持对该股的买入评级,并将 3 月 18 日投资者日的目标价定为 58 美元。除了对各个终端市场的更新外,公司预计管理层将重点介绍光学部门业务,该业务受益于长期和周期性需求趋势,且运营商对光纤的需求正在回归正常建设趋势。花旗认为,鉴于康宁需求的改善和自由现金流生成潜力,其风险/回报比显得有利。

Reuters: 路透社:

Tesla (TSLA.O),is working with Chinese tech giant Baidu to improve the performance of its advanced driving assistance (ADAS) system in China, two people with knowledge of the matter said, after a recent update drew customer criticism.

特斯拉(TSLA.O)正在与中国科技巨头百度合作,以提升其在中国的高级驾驶辅助系统(ADAS)性能,两位知情人士透露,此前的一次更新引发了客户批评。Baidu dispatched a group of engineers from its mapping team to Tesla's Beijing office in recent weeks to work on better integrating Baidu's navigation map information, such as lane marking and traffic light signals, with Tesla's Full Self-Driving (FSD) Version 13 software, the sources said.

消息人士称,百度最近几周派遣了一批来自其地图团队的工程师前往特斯拉北京办公室,致力于将百度的导航地图信息(如车道标记和交通灯信号)更好地与特斯拉的全自动驾驶(FSD)第 13 版软件集成。

Loop recently met with Palantir CFO David Glazer and finance team members, viewing an AIP product demonstration and discussing AI industry trends, competition, spending direction, and Palantir's "bootcamp" go-to-market model. While the meeting was primarily introductory, Loop says they came away with increasing conviction in their Buy rating and core investment thesis that Palantir is an early software leader in enterprise AI. Loop believes the industry is at a tipping point as small-scale pilot programs move into production environments and AI use cases grow exponentially across all industries.

Loop 最近会见了 Palantir 首席财务官 David Glazer 及其财务团队成员,观看了 AIP 产品演示,并讨论了人工智能行业趋势、竞争、支出方向以及 Palantir 的“训练营”市场进入模式。虽然此次会议主要是介绍性质的,但 Loop 表示他们对 Palantir 作为企业 AI 领域早期软件领导者的买入评级和核心投资论点更加坚定。Loop 认为,随着小规模试点项目进入生产环境,AI 用例在各行业中呈指数级增长,该行业正处于一个转折点。

SMCP:

Tesla has received massive orders for its refreshed Model Y SUV in mainland China, a major boost for the US electric vehicle (EV) maker after sales fell sharply last month.

特斯拉在中国大陆收到其改款 Model Y SUV 的大量订单,这对这家美国电动汽车制造商来说是一个重大提振,此前其上月销量大幅下滑。The company’s Gigafactory in Shanghai, its largest in the world, is ramping up production of its bestselling model to ensure early deliveries to customers, according to two sales managers in the city.

该公司位于上海的超级工厂,作为其全球规模最大的生产基地,正加速其畅销车型的生产,以确保尽早交付给客户,据该市两位销售经理透露。Tesla’s sales on the mainland in February fell to 30,688, the lowest since July 2022. Deliveries slumped 51.5 per cent month on month and 49.2 per cent year on year.

特斯拉 2 月份在中国大陆的销量降至 30,688 辆,为 2022 年 7 月以来的最低水平。交付量环比下滑 51.5%,同比下滑 49.2%。

Stock sold off into the close yesterday as mgmt didn’t change the LT model (20%+ OPM, 25%+ FCF mgn), they pushed out $5B rev run rate goal to 2028 from 2027 (initially provided in 2022) although street only at $4.5B. NET expressed comfort that it can grow annual revenue in line with 2024 growth (~28%-29%) for another few years.

昨日股票在收盘时遭遇抛售,原因是管理层未调整长期模型(20%以上的营业利润率,25%以上的自由现金流利润率),并将 50 亿美元营收目标从 2027 年推迟至 2028 年(最初于 2022 年提出),尽管市场预期仅为 45 亿美元。NET 表示有信心在未来几年内保持与 2024 年相近的年度收入增长率(约 28%-29%)。

While KEYB's carrier survey was slightly positive, its Key First Look Data results were disappointing with sell-through -6% y/y. its carrier surveys indicate iPhone 16 sell-through in February was slightly better than store expectations and normal seasonal trends. Demand for the iPhone 16 PRO/MAX remained relatively healthy, while demand for base models were relatively weaker. Feedback on the iPhone 16e was disappointing due to its higher price point and lack of compelling specs. Apple AI remained a non-factor in driving near-term demand. KEYB views its Febraruy carrier survey and KFL results as neutral for the Apple supply chain

尽管 KEYB 的运营商调查结果略显积极,但其 Key First Look 数据结果令人失望,同比销售下降 6%。其运营商调查显示,iPhone 16 在 2 月的销售略好于门店预期和正常季节性趋势。iPhone 16 PRO/MAX 的需求保持相对健康,而基础型号的需求相对较弱。由于价格较高且缺乏吸引力的规格,iPhone 16e 的反馈令人失望。苹果 AI 在推动近期需求方面仍无显著影响。KEYB 认为其 2 月运营商调查和 KFL 结果对苹果供应链而言为中性。

Consumer: Consumer Angst Is Striking All Income Levels - WSJ

消费者:消费者焦虑正在影响所有收入水平 - 《华尔街日报》

AMZN: FTC backtracks earlier statement regarding limited resources for Amazon litigation; says has no resource constraints

AMZN: FTC 撤回早前关于亚马逊诉讼资源有限的声明;表示没有资源限制

GOOGL: Google Debuts AI Model for Robotics, Challenging Meta, OpenAI – Bloomberg

GOOGL: Google 推出机器人 AI 模型,挑战 Meta、OpenAI – Bloomberg

MSFT: as reported midday Wed, the FTC will proceed w/ its broad antitrust probe on MSFT – Bloomberg

MSFT:据彭博社周三午间报道,FTC 将继续对 MSFT 进行广泛的反垄断调查

OpenAI: OpenAI exec reveals the tech giant’s ‘biggest challenge’ right now – CNBC

OpenAI 高管揭示科技巨头当前面临的“最大挑战”——CNBC

JPM on Positioning:

HF performance started to recover on Tues as momentum / crowding performed much better. HF crowding has seen sharp declines in the past month that are getting close to some of the worst we’ve seen in the past few years in both N. Am. and EMEA. These would suggest much of the move could be over. However, gross flows have not shown nearly as extreme a move (beyond 1wk de-grossing in EMEA that is very large). Gross leverage remains elevated, but starting to tick lower.

对冲基金(HF)表现于周二开始复苏,因动量/拥挤策略表现显著改善。过去一个月中,HF 拥挤度急剧下降,接近北美和欧洲、中东及非洲(EMEA)地区过去几年最糟糕的水平。这表明大部分调整可能已经结束。然而,总资金流动并未显示出如此极端的变动(除了 EMEA 地区一周内的去杠杆化,规模非常大)。总杠杆率仍处于高位,但开始逐步下降。

Colgate at UBS conf yesterday on consumer weakness (h/t Citi):

高露洁在昨日 UBS 会议上关于消费者疲软的讨论(来自花旗的消息):

“Now that has obviously been further impacted this year by the slow start to the categories in the US that we've talked about in Mexico, that slowdown that we've talked about over the past couple of quarters and we're seeing that sort of filter through across the businesses right now. as we look at the underlying trends, what's really changed, I think is the slowdown in consumer demand that we've seen over the past couple of months. That was obviously the big topic of conversation at CAGNY. As we're looking at a consumer that is a little bit more cautious in dealing with issues like perception of higher inflation, what's going on with layoffs, what's g on with the Hispanic consumer, et cetera? And then as it came up at CAGNY, sort of how that plays out into what's going on with retailer destocking, et cetera. So I think we're seeing that right now. That's having an impact on category growth. We're seeing that spread a little bit, I think, to some other countries in terms of looking at Mexico and Central America, Europe seems to be hanging in. So I think as we look at this, we have -- we expected a category deceleration. I think as you look at the first quarter, that's happening a little more rapidly than what we had anticipated and we just need to see how that plays out over the next six to nine months.”

“显然,今年这一情况因我们在墨西哥讨论过的美国品类起步缓慢而进一步受到影响,这种放缓在过去几个季度中我们已有所提及,目前我们正看到这种影响逐渐渗透到各业务中。当我们审视潜在趋势时,我认为真正改变的是过去几个月我们所见的消费者需求放缓。这显然是 CAGNY 会议上的主要讨论话题。我们观察到的消费者在处理诸如对高通胀的感知、裁员情况、西班牙裔消费者的反应等问题时显得更为谨慎。随后,在 CAGNY 上,这一问题又延伸到了零售商去库存等现状。因此,我认为我们目前正目睹这一现象,它对品类增长产生了影响。这种影响似乎也在向墨西哥和中美洲、欧洲等其他一些国家扩散,尽管欧洲似乎还在坚持。所以,在我们看来,我们预期到品类增长会有所减速。 我认为,当你审视第一季度时,情况比我们预期的进展稍快一些,我们只需观察接下来六到九个月将如何发展。Regarding the US specifically: “Yeah, I think it's relatively broad based. I think what we're seeing is a little bit of a reduction in traffic. I think we're seeing, again, some hesitancy in the consumer given all the news flow that’s going out there.

关于美国的具体情况:“是的,我认为影响相对广泛。我们看到流量略有减少。我认为,鉴于当前的各种新闻报道,消费者表现出一些犹豫。”