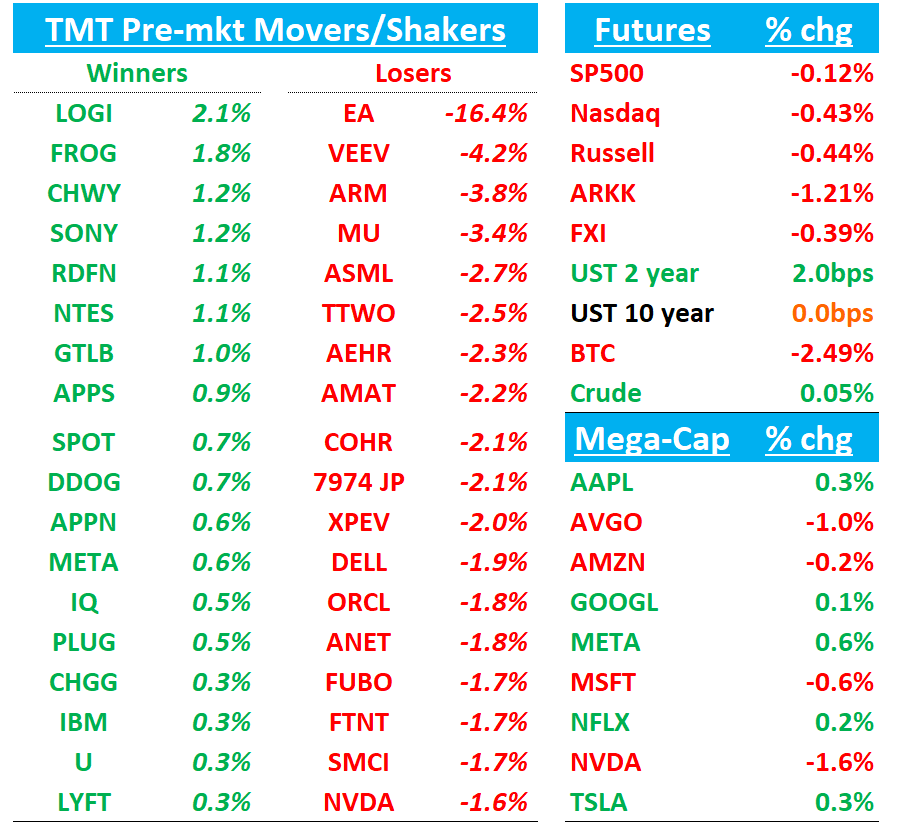

TMTB Morning Wrap

QQQs - 42bps giving back some of yesterday’s gains. A bit of shine coming off of Stargate this morning as doubts around funding continue. Yields flat to up. BTC - 2.5% getting back close to $100k. Let’s get to it….

OpenAI, SoftBank Each Commit $19 Billion to Stargate Data Center Venture

Details coming out on Stargate…

OpenAI and Japanese conglomerate SoftBank will each commit $19 billion to fund a joint venture to develop data centers for artificial intelligence in the U.S., OpenAI CEO Sam Altman told some colleagues Wednesday.

The ChatGPT developer would effectively hold a 40% interest in the venture, Stargate, and it would act as a kind of extension of OpenAI, he said. Stargate stems from Altman’s longtime concern about his company’s access to servers as it faces rising competition from Elon Musk and others. Altman’s comments imply SoftBank would also have a 40% interest.

Altman’s comments on Tuesday suggest the company will have to raise $19 billion through equity or debt, and company leaders previously told colleagues they were prepared to raise debt for data center projects. The company projected to generate about $4 billion in revenue last year while still burning considerable sums of cash due to high computing costs

Semi analysis also out on Stargate. Their take is MSFT biggest loser as “this is incrementally negative for MSFT long term since they were afraid to take on the risk of this investment…we don’t think short-term benefit off less capital intensity outweighs long run potential harm of losing rev and control over OpenAI”

NFLX: Wolfe upgrades to Buy

Wolfe Research upgraded Netflix to Outperform from Peer Perform with a $1,100 price target following the Q4 earnings report. The company's "superior scale" led to accelerating financial returns and expanding potential to capture the long-term total addressable market, the analyst tells investors in a research note. The firm says Netflix's results and 2025 guidance "buried" its long-standing concerns about a deep slowdown after the 2023-2024 "barrage of password sharing interventions." The company's widening growth strategies, superior scale, and "rich" cash flow position it to extend its lead in long-form video streaming, which continues to take wallet share from pay TV, a $130B revenue category in the U.S. alone, contends Wolfe. The firm thinks "it could be a very, very long time before Netflix reaches a terminal growth rate."

META: Clev out positive saying Q4 likely better than expected driven by upside in DR spend in retail/ecom. Sees accelerating growth vs Q3 (street at 17% Q4 vs 19% Q3)

DDOG BAH added to BOFA US 1 list

MU -3% / Hynix -3%: Hynix results ok but warned of steeper demand declines in commodity memory chips although said HBM sales would more than 2x this year.

Revs came in a bit below buyside expects. Notably weaker NAND results with bits down MSD% QoQ vs +L-Teens QoQ guide, and softer 1Q DRAM bits guide at down L-Teens QoQ. Semi cap stocks also hit a bit as Hynix posting a more modest capex spend plan for 2025 than expected : “The construction of these new fabs will lead to a marked increase in infrastructure-related investment this year, though overall investment increment will be limited.” CFO Kim Woo-hyun noted risks tied to trade protectionism and geopolitical tensions, with inventory adjustments further pressuring demand. All in all, seems ok given positive HBM commentary - everyone knows about NT NAND/DRAM weakness.

Details:

Operating Profit: ₩8.08T (Est. ₩8.03T) Net Income: ₩8.00T (Est. ₩5.91T) Revenue: ₩19.77T (Est. ₩19.77T)

Outlook:

1Q 2025 DRAM B/G: Low-teen% decrease QoQ

1Q 2025 NAND B/G: High-teen% decrease QoQ

2025 DRAM Market Outlook: Mid-to-high teen% growth

2025 NAND Market Outlook: Low-teen% growth

HBM Revenue: Expected to grow over 100% YoY in 2025

Q4 Segments:

HBM Revenue: Over 40% of total DRAM revenue in Q4, with HBM3E shipments beginning as planned.

DRAM ASP: Increased +10% QoQ due to a favorable product mix (HBM and DDR5).

NAND Revenue: Growth driven by enterprise SSD (eSSD) demand, though legacy products like DDR4 saw price declines.

EA -15%: Negatively pre announces Q3’25 and FY25

Bookings guide was revised down considerably, 8% below street. EA cite player engagement shortfalls in EA Sports FC 25 and Dragon Age (50% lower than expected engagement). The implied guide for Q4’25 goes down by 18% as FC and general live services weakness is expected to continue into the end of the year. Pretty big surprise as most thought EA sounded v positive at their Sept analyst day where they talked bullishly about growth over the next few years.

Bears will say core IP has lost traction with weakness in their co flagship titles (FC potentially in structural decline), mgmt has completely lost credibility, GTA overhang, not cheap on new numbers (18x P/E) and battlefield no where in site. Not much for bulls to hang onto.

Gets a downgrade at Raymond James, BAML and BMO this morning.

3P Roundup:

RBLX: Slight downtick on weekly data

ETSY/CHWY: Uptick in Weekly data at Yipit

VEEV: GS double downgrades to Sell from Buy - lowers PT to $200 from $261

According to Goldman Sachs: While Veeva maintains strong positioning in Life Sciences with long-term cross-selling potential, several key risks exist: 1) Salesforce's competitive pressure in Commercial space may impact sentiment despite Veeva's superior offering 2) Life Sciences sector recovery appears gradual, with customer cost management likely affecting deal momentum 3) Portfolio maturation makes meaningful growth acceleration from newer products like CDMS challenging.

PLTR: Wedbush raises PT to $90 from $75, saying AI Strategy Positions PLTR as “core winner”

Wedbush raised their Palantir price target to $90 from $75, citing growing conviction in the company's AI strategy as central to their 2025 thesis. The firm sees Palantir evolving into a potential Oracle or Salesforce-caliber company. Despite rich valuation, Wedbush views what they call the 'Messi of AI' as positioned to capture significant share of upcoming AI spending waves. Their analysis shows both new and existing customers across commercial and federal sectors actively pursuing Palantir's technology stack as the company rolls out additional AI use cases. Wedbush analysts believe the market is significantly undervaluing the potential of Palantir's AIP commercial business, which they project could generate over $1 billion in revenue, while also underestimating the competitive moat developed under Karp's leadership.

LOGI: MS upgrades to Hold after thesis plays out

With MSCO's prior UW thesis having largely run its course, it is upgrading LOGI to Equal-weight. Since the end of May '24, the two most important factors underpinning MSCO's prior LOGI downgrade to UW have played out. First, Consensus long-term revenue growth expectations have converged closer to MSCO's view, with the Street now forecasting a 4% revenue CAGR through 2027, just 100bps above its current forecast. Second, on the back of these negative revisions, LOGI's P/E multiple has de-rated by 4x turns, significantly underperforming MSCO's IT Hardware group that has re-rated by 1x turn, and the market multiple that has re-rated by 2x turns.

FTNT: Fortinet revenue guidance could miss consensus, says Deutsche Bank

Deutsche Bank maintains a Hold rating and $85 target on Fortinet, expressing caution ahead of 2025 guidance. They expect investors to focus on whether the hardware refresh cycle can drive growth beyond the 12% mid-term target discussed at November's analyst day. The firm's skeptical stance on industry refresh potential and Fortinet's continued reliance on hardware firewall sales leads them to anticipate potential below-street revenue guidance. Deutsche Bank suggests this could disappoint given the stock's 75% rise since Q2 results.

META: BAML previews the quarter and lays out positive vs negatives for the stock - raises PT to $710 fro $660

Bulls point to: AI-driven ad targeting improvements boosting ROI and spend; growing business messaging adoption and monetization; untapped revenue from Threads, Marketplace, and Meta AI; potential TikTok share gains; and margin expansion from cost controls including 5% headcount cuts.

Bears focus on: Revenue growth deceleration impacting valuation; capex pressure on FCF/margins; policy risks (pharma ads, tariffs, Section 230); regulatory threats (FTC case, teen targeting, DMA); rising competition from TikTok, eCommerce, and streaming platforms. Above-average P/E multiple adds valuation risk.

PANW: Barclays out trying to reconcile why billings is less indicative of cash collections and why they think 37% FCF margins is doable

Barclays addresses PANW's recent underperformance and concerns about 37%+ FCF margin guidance amid negative billings growth. They defend the FCF target through three key points:

Shift from PAN FS deals to annual-in-advance billing affects billings but not cash collections

20-25% of business could transition to annual payments gradually, with operating margin expansion providing FCF protection

Declining financing receivables from fewer PAN FS deals could boost FCF, offsetting lower deferred revenue

The firm suggests billings have become less relevant as a metric given these structural changes in PANW's business model.

RBLX: Cowen slightly more positive on end of Q4 3p data

Cowen tracks two Roblox bookings projections: app store analysis suggests $1.32B (+17% q/q), below consensus of $1.36B but up from November's $1.29B estimate. Strong December performance followed the "Dress to Impress" update. Their RMS analysis points to $1.36B, at guidance's high end (±$40MM range). They expect Q4 guidance achievement with upside potential, though note gift cards represent 20%+ of Q4 bookings - a channel poorly tracked by third-party data.

CRWD PANW ZS FTNT: ISI says partners bullish S, PANW and FTNT but mixed on CRWD

Partners have exceeded expectations for PANW, ZS, and FTNT while CRWD struggles with underwhelming performance, ISI reports. Pipeline momentum has surged for ZS, with 84% of partners projecting accelerated growth versus 50% last quarter, representing a 17% increase in momentum. ISI says CRWD faces a mixed recovery ahead of its high-renewal quarter, noting end of Q4 diverged from Q3 trends with “pipeline feedback tilting towards underperformance.” Despite competitive pressures, ISI observed improved Q4 pricing power, especially for PANW and ZS. Their analysis indicates potential firewall refresh momentum building for 2H, supported by increased CISO prioritization. Sequential pipeline deterioration was noted for TENB, CYBR, and RBK.

DASH: Home Depot a big addition for New Verticals; raising PT to $205; Reiterate Buy at BAML

DASH added $HD as a partner, with over 2,000 stores nationwide coming to the platform for delivery. If 5% of HD's digital sales were to shift to DASH, that could contribute 160bps to DASH GOV growth. With multiple data points suggesting strong top-line trends for DASH, BAML is raising its PO to $205 based on SOTP

ByteDance plans $20 billion capex in 2025, mostly on AI, sources say

ByteDance, the Chinese owner of TikTok, has earmarked over 150 billion yuan ($20.64 billion) in capital expenditure for this year, much of which will be centred on artificial intelligence, two people briefed on the matter said.

The privately held technology giant plans to spend about half of the amount abroad on AI-related infrastructure, primarily data centres and networking equipment, they said.

The main beneficiaries of the spending will be chipmakers Huawei Technologies (HWT.UL) and Cambricon Technologies (688256.SS), opens new tab plus U.S. supplier Nvidia (NVDA.O), opens new tab, the people said, declining to be identified as the information was confidential.

BKNG ABNB EXPE: JMP previews travel, saying strong USD may drive intl upside for BKNG

Similar to recent quarters, upper-funnel trends continued to be mixed in Q4 while industry trends remained resilient, suggesting durable travel demand. Additionally, JMP notes Consumer Confidence improved q/q, though it remains relatively range bound below pre-pandemic levels. JMP expects investors will be focused on market share dynamics, particularly in the U.S. and within alternative accommodations; 3P data suggests BKNG took or maintained share in Q4. Further, JMP says investors will look for color around investment levels and profit margins heading into the new year with BKNG announcing a cost reduction plan, EXPE investing behind Vrbo and international markets growth, and ABNB expanding beyond the core. While the macro environment remains uncertain in the near term, JMP views BKNG as the stock to own within online travel given its relatively durable upper-funnel trends, share gains in the U.S. and in alternative accommodations, a USD dynamic that either creates more international travel or drives FX tailwinds

TSLA: Oppenheimer comments saying they continue to see risk in Trump/Musk relationship

Oppenheimer expects Tesla to pivot focus toward Physical AI while tempering 2025 vehicle growth expectations under the pretext of Model 2 and autonomous vehicle development. The firm seeks details on system validation and AI model optimization for autonomy as key progress indicators. Oppenheimer warn of risks in the Trump/Musk relationship potentially threatening Tesla's benefits. Citing weakening US and EU demand, Oppenheimer maintains caution on Tesla's fundamentals and competitive position in autonomous technology.

Also: TSLA will raise prices of all its cars in Canada from Feb. 1, according to notices on its Canadian website, with prices of Model 3 going up by as much as C$9,000 ($6,254.78). Model Y variants will see increases of up to C$4,000, while all versions of Model S and X will rise by C$4,000, according to the website.

Other News:

AAPL, GOOGL: UK's CMA to investigate Apple and Google's mobile ecosystems – CMA

iPhone, Xiaomi prices cut in China to reap smartphone subsidies – Nikkei Asia – link

Agencies: WPP has looked at switching primary listing to New York as it pursues opportunities in US under new Trump administration – FT

CHWY: Upgraded to Buy from Hold at Argus

EVs: EU plans subsidy for electric vehicle sales to counter China - FT

Gen AI: TikTok parent ByteDance denied the report that it will spend >$12B on AI in 2025, including $5.5B on AI chip purchasing and $6.8B investment on overseas AI model training programs – ijiwei

MSFT: OpenAI’s Stargate Deal Heralds Shift Away From Microsoft - WSJ

Media: CNN to lay off hundreds of employees as post-inauguration transformation begins, sources say – CNBC

Stargate: Musk Pours Cold Water on Trump-Backed Stargate AI Project – WSJ – link

Memory: Nvidia Partner SK Hynix’s Profit Fails to Impress AI Chip Bulls– Bloomberg

Memory: TrendForce reports NAND manufacturers, including MU, Kioxia/SanDisk, Samsung and SK Hynix/Solidigm plan to cut production in 2025 to ease supply-demand imbalance and stabilize prices – link

PYPL: Chief Product Officer John Kim to depart company on March 31st

Samsung: co. unveiled its Galaxy S25 smartphone with personalized AI assistant; also plans to launch an ultrathin version in 1H this year, pricing lower than $1299