No, Jerome Powell Isn’t Playing Politics

The Federal Reserve has demonstrated that it is relying on data to make interest-rate decisions.

Policy, not politics.

Photographer: Chip Somodevilla/Getty Images

To get John Authers’ newsletter delivered directly to your inbox, sign up here.

Today’s Points:

- Despite appearances, Jerome Powell probably isn’t playing at politics;

- But that won’t convince the skeptics that the Fed isn’t propping up the stock market;

- There are legitimate questions over central bank independence;

- A presidential campaign isn’t the best place to air those questions

- AND happy 98th birthday to the great David Attenborough

Powell’s Staying the Course

Investors’ hopes for rate cuts this year have faded. The past quarter’s economic data showed that the inflation battle is not over; whether the Fed eases now depends on the data, a point Jerome Powell and the Federal Reserve have repeated ad nauseam. Then came last week’s nonfarm payrolls data for April, it was cooler than expected, and that was enough to re-establish hopes that cuts are back on the table — although investors still don’t expect the first cut until November, according to the Bloomberg World Interest Rate Probability function.

That would mean delaying until just after the intensely competitive US presidential election — and it’s no surprise that the Fed’s policy initiatives are being viewed ever more through a political lens. Conservatives have been forthright in their criticisms of the Fed in a manner that raises questions about whether the Fed would maintain its independence under a second Trump administration.

There are legitimate reasons to question central banking independence as it currently operates; when Powell was renominated as Fed chair, this column’s headline was The Fed Has Risen Too Far Above Political Control. But tinkering with its status needs to be done with great care, as it risks ratcheting up uncertainty and thus disturbing capital markets. And beyond that, it’s hard to overstate the usefulness of an independent central bank. The end of the dollar’s tie to gold in 1971 led to a period of savage inflation. Prices only came under control after the Fed, under Paul Volcker, proved itself willing to force a recession. Since then, a fiercely independent central bank has come to be seen as essential to maintaining confidence in the currency. But there will be no lack of politicization claims should the Fed decide that the data permit the loosening of policy ahead of the election after all. Gavekal Research's Will Denyer argues he doesn’t see the Fed departing from its data-dependency stance:

Can the Fed change rates right before the election? The short answer is they’ve done it many times before. Would Powell, all else equal, prefer not to change rates right before the election? Probably. I don't think that preference is as strong as some people think. He’d prefer it, but he can do it if the data calls for a cut or a hike. Will the data call for a cut or a hike before the election? That’s the big question.

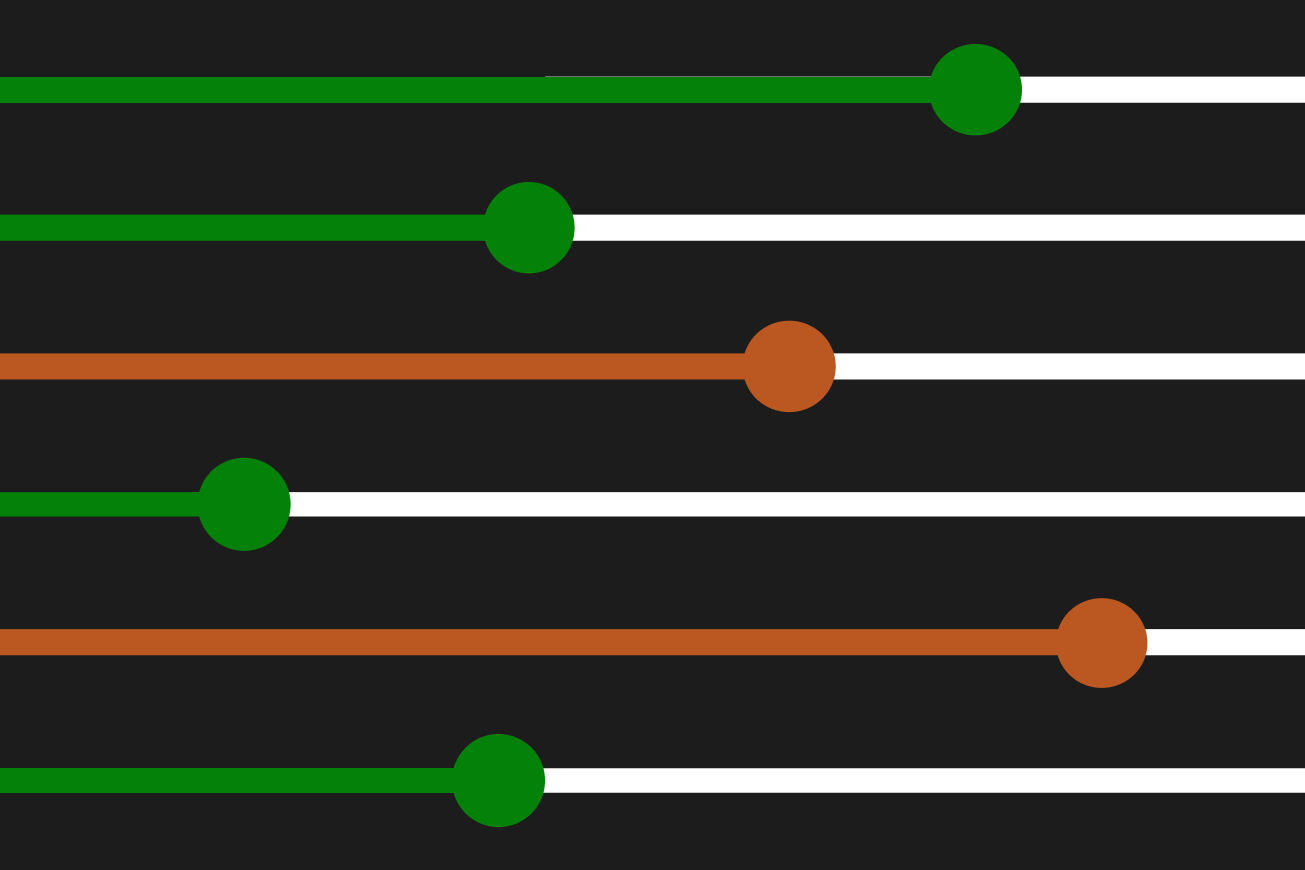

The central point, according to Denyer, is that what appeared to be a clear disinflationary trend last year, which appeared to justify cuts, has been followed by an inflation rebound. This Gavekal Research chart shows Fed’s policy actions in the run-up to previous elections.

Powell can’t stress enough the importance of the Fed’s independence. As he mentioned in a recent address at Stanford University, this independence enables and requires the Fed to make monetary policy decisions without considering short-term politics. Ordinarily, this should be the end of the story. But it’s not the case. The Fed’s independence is now on the political agenda, which will inevitably color perceptions, and as always a central bank’s decisions have the potential to damage political fortunes. So the Fed has been dragged into partisan conversations, and will remain in them for at least the next six months.

The Fed’s strong protest of innocence hasn’t warded off prying eyes into its mandate. Powell took a startlingly dovish pivot in December. That fueled the market’s expectations of easing ahead, and instantly pushed down longer-term rates. But Marko Papic, a macro strategist at The Clocktower Group, suggests that the Fed is “politically motivated to stay behind the curve” and that the pivot was a move to help Joe Biden:

It's not like they need to cut to be political – it's about ensuring that their mindset is focused on stability and growth and taking left tail risks off the table. Like Silicon Valley Bank, that's what they're focused on rather than on their mandate, part of which is inflation, obviously. That's why I say they’ve pivoted towards leniency. They're not as stuck on inflation. They're willing to see inflation be sticky, perhaps for a pretty long time. And they're not really concerned about getting inflation under 2% anymore. They've kind of abandoned that for the 12 months ahead of the election. That's the political nature of them.

Some analysts interpreted the December pivot as a new “Fed put” — and thought Powell’s latest press conference after the recent Federal Open Market Committee could be seen as the clincher. It is difficult to explain what a Fed put would look like without resorting to even more jargon. The Macro Compass’ Alfonso Peccatiello does a better job by summing it up as a situation where the monetary policy authority would “have the market’s back,” and investors would know that at any sign of market weakness, a big easing would be around the corner. But when the economy or inflation accelerated, the Fed wouldn’t react hawkishly but rather “let the economy run hot.” It was originally known as the “Greenspan Put” after the federal funds rate seemed to be rising and falling in response to the stock market during Alan Greenspan’s last decade as Fed chairman:

In the quarter century since people started talking about a Greenspan put, even more of Americans’ wealth is packed in pension funds, and indexes now ensure that everyone knows immediately when their holdings lose money. Hence any market downturn would incur voters’ displeasure. That, the cynical argument goes, prompts the Fed to bolster the stock market.

So far this year, the markets seem to be doing fine — nothing is broken yet, very much what the Fed wants. Many will read party politics into this, particularly when the challenger to the incumbent has plans to limit the Fed’s independence, which we can assume its governors want to avoid. But that’s not a sufficient basis for calling the credibility of the Fed into question. As Tom Porcelli, chief US economist at PGIM Fixed Income, argues, Powell’s team has demonstrated their reliance on data and isn’t swayed by anything that opens them to a political attack. After all, any misstep will prove not only costly to his legacy but to the Fed as an institution.

It’s very easy for people to want to go down the path of trying to make this about political development. But what if it’s worse? What if the Fed just really have a really bad angle on what's happening from an economic perspective? I always find it funny or interesting that it always comes down to politics.

It’s in the market’s interest that the Fed stay independent and its credibility intact. But there is very little it can do to prevent some of these aspersions, even if it wants to. The key focus through all this would be to keep to their word and be as proactive as possible. And in that regard, they have not done a bad job.

-- Richard Abbey

Survival Tips

Happy birthday David Attenborough, who turns 98 on Wednesday. He’s probably Britain’s most popular person, and deserves to be. If anyone is a legend in his own lifetime, it’s him. His nature documentaries never grow old. Try this, and this, and this.

More From Bloomberg Opinion:

- Gaza Cease-Fire Should End With Hamas’ Exile: Marc Champion

- No, Low-Skilled Immigrants Don’t Cost Taxpayers Money: Tyler Cowen

- Apple Needs to Move the iPad Beyond the Toddler Stage: Dave Lee

Want more Bloomberg Opinion? OPIN <GO>. Or subscribe to our daily newsletter.

— With assistance from Richard Abbey

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.