TMTB EOD Wrap

Good afternoon - QQQs +15bps as treasuries got hit hard today with yields up 7-10bps across the curve and 10 year hitting 4.2%, which hit some rate sensitive names such as housing and telco stocks. China also some more profit taking with FXI -1.5%. The market is now pricing in 42bps worth of cuts over the last two FOMC meetings of the year w a 90% probability of a 25bp cut on 11/7. Despite SOX being flat, NVDA +4% followed TSM with 2nd large cap AI semi to hit 52wk high - MRVL and AVGO not far behind, which bodes well for the QQQs

Let’s get to the good stuff…

Internet

NFLX +1% follow through from Friday as investors like the catalyst set up heading into Q4: Paul/Tyson fight in Nov; Squid Games 2/ NFL live around Christmas; pricing increase; and WWE Raw launching in Jan. 3P data so far looks solid in Q1

Other large cap mixed: GOOGL +3bps; AMZN flat as UBS dug into Kuiper investments; and META - 40bps

Rate sensitive names hit: RDFN - 8.5%; Z - 1.3%; OPEN -2%; W - 9%

CVNA flat…3p data looking like another accel last week to mid 50s unit growth - will likely get confirmation from Yipit tomorrow.

EXPE +2% after a positive write up at Barrons. Other travel names o/p: UBER +1.7%; ABNB +40bps

Midcap weak on the day: RDDT -2.5%; ROKU -4%; CHWY -5% as 3p data not looking so great in Q3; MTCH -1.6%; PINS -70bps

SPOT +75bps as M-sci cancellations remain healthy

RBLX +1% as 3p data continues to track ahead in Q3

Semis

NVDA +4% to ATHs as Commercial times said MSFT increasing orders for GB200

MRVL +2.4% as Trendforce reported they are going to raise prices on optics next year given strong AI demand

MU - 2% new short idea at Hedgeye

AVGO -40bps continues to lag a bit after NDR last wk with BAML where they said Q1 non-AI was going to be “seasonally flat to down” vs street modeling up low MSD

Other AI names o/p: AMD +1.2%; TSM +40bps; ANET +80bps

Analog mixed: ADI - 1.2%; ON - 2%; MCHP - 3%

Software

NOW -80bps handling the MS downgrade ahead of earnings pretty well

MSFT -20bps / CRM - 80bps as MSFT unveiled 10 new AI agents for enterprise focused Dynamics 365 apps covering sales and finance ahead of CRM Agentforce going GA this week…Also more talk of OpenAI/MSFT partnership and what that means going forward (WSJ)

DDOG -2% as Bernstein slashed numbers based on recent checks saying non-tech enterprises taking longer to rollout Gen AI

FTNT +1.2% as MS made a top pick…PANW +60bps as MS was also positive

GTLB flat on Needham’s upgrade

APP +10% continues to rip to new highs

Elsewhere

AAPL +45bps as JPM said IP16 lead times now tracking in linen with IP15 and Loop raised iPhone #s based on their supply checks

HOOD +50bps as sell-side came away positive on their Summit and higher rates helps them

Other fintech mixed: PYPL -60bps; SQ - 1%; AFRM - 2%; COIN - 2.3% on BTC -1.5% weakness

TSLA - 1%

Solar names weak with higher rates: RUN -6%; FSLT - 2%; ENPH -1.3%

XPEV +3% as JPM added positive catalyst watch

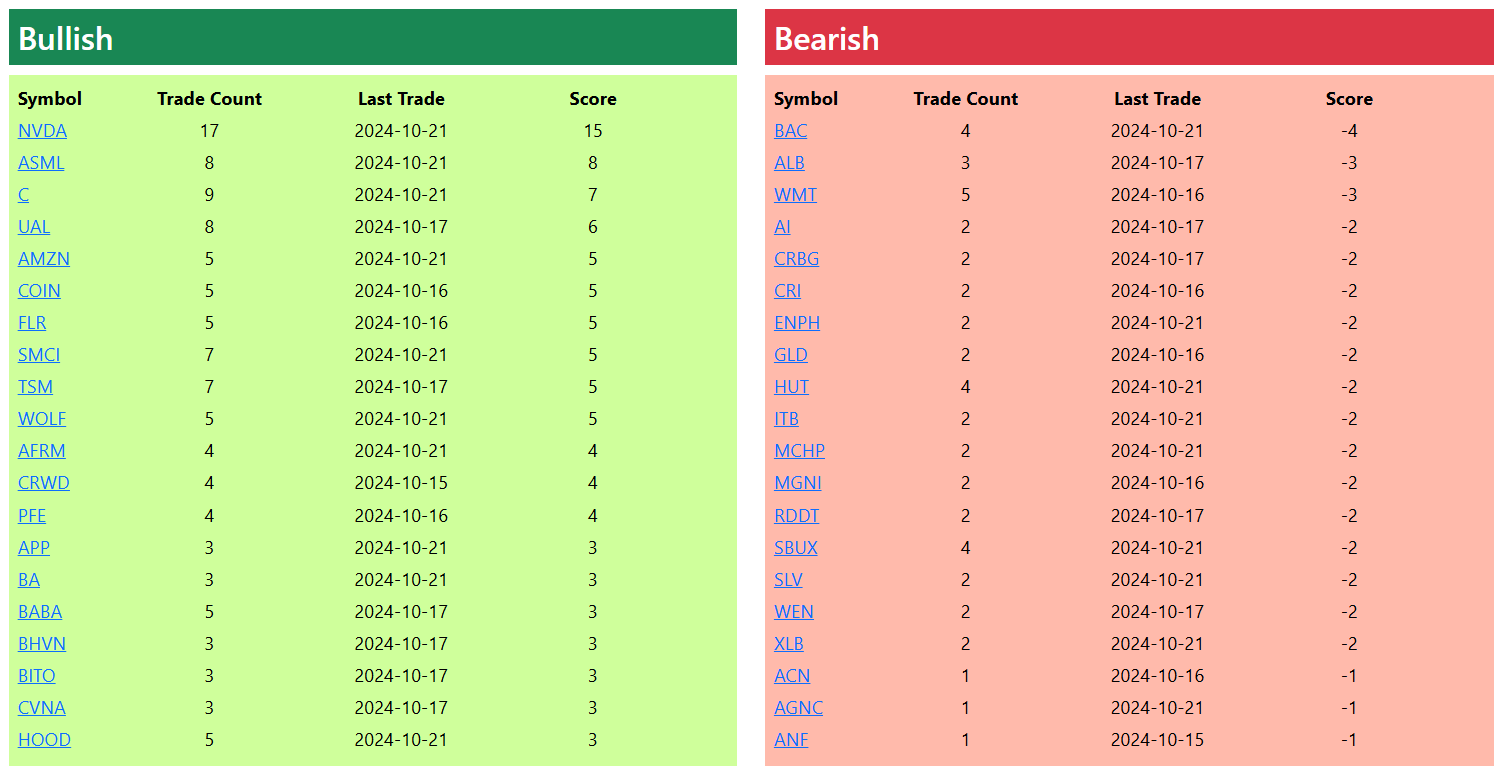

Bullish and Bearish Weekly Option Flow